BLOG

Construction & Real Estate Insights

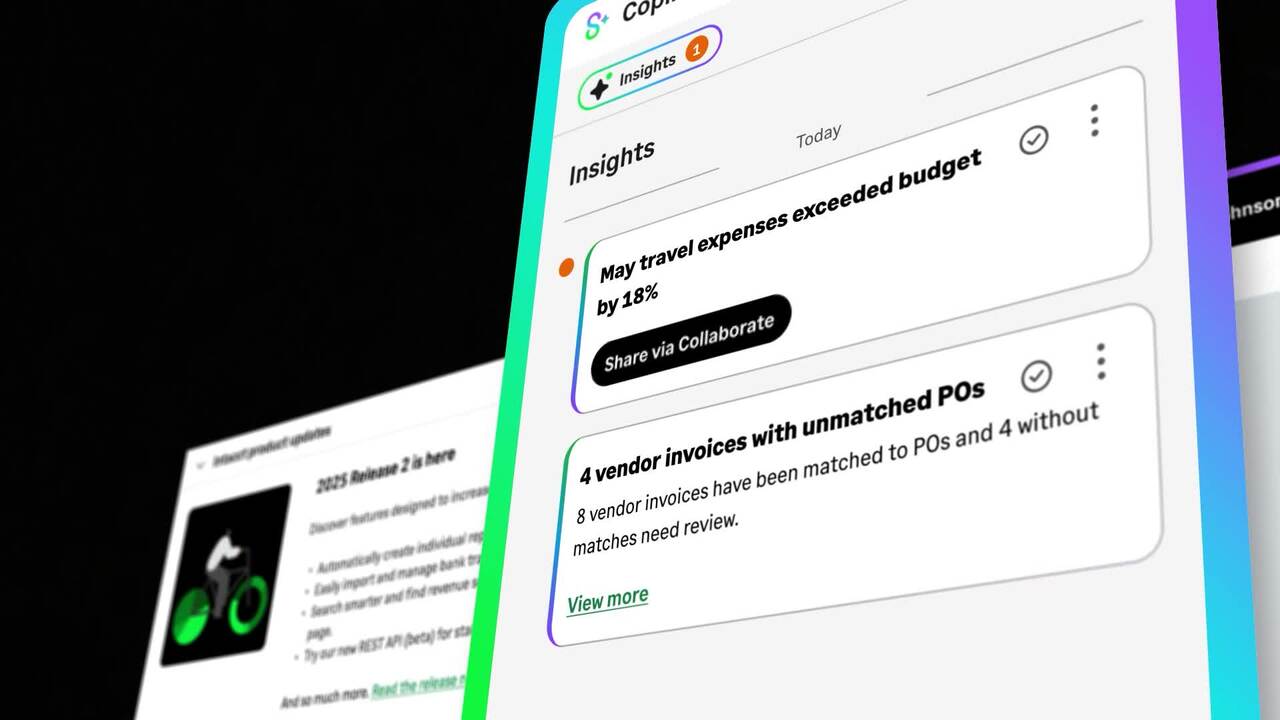

What Sage Copilot Actually Does and Why Construction and Real Estate Teams Should Pay Attention

Blog Posts

What GCs Are Watching in 2026: Labor, Tariffs, and AI

What General Contractors Are Watching in 2026: Labor, Tariffs, and Where AI Is Actually Showing Up

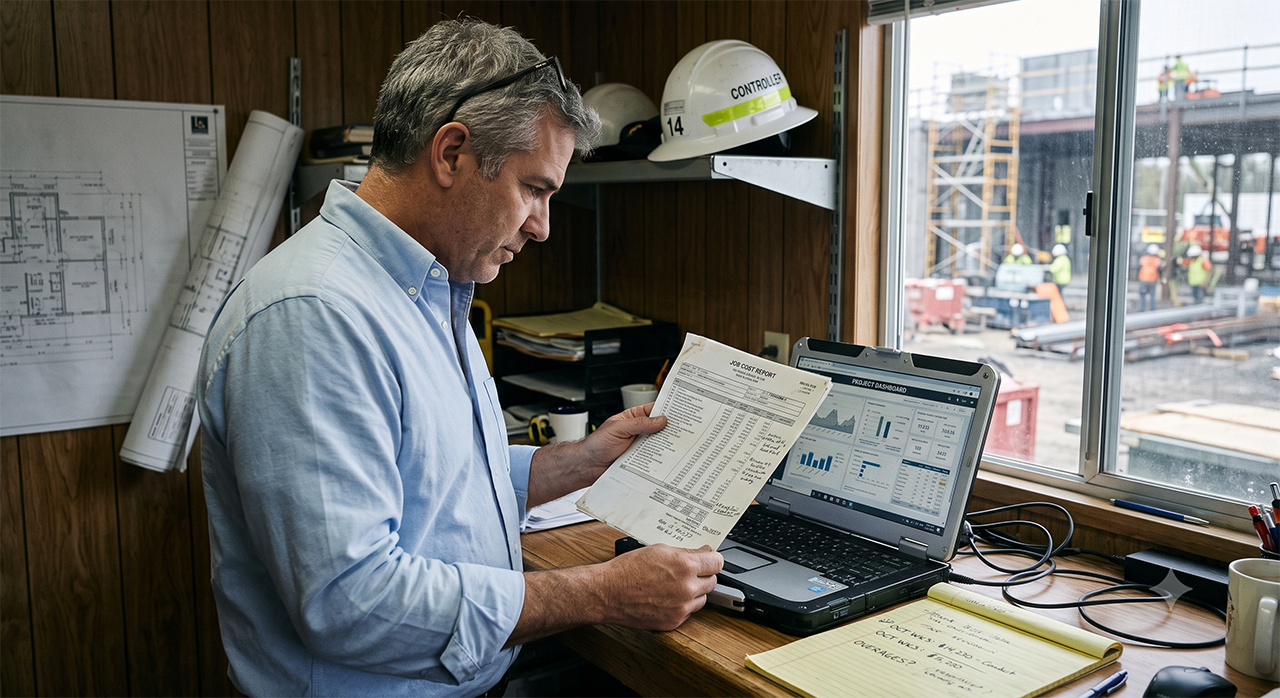

A construction CFO sits down for a Monday leadership meeting. The agenda is familiar. Backlog is solid. Margin pressure is real. Two jobs are running tight. The team is short three estimators and a controller. Tariff costs on steel and electrical components shifted again last week. The AI tools the COO has been testing for six months are starting to produce real numbers in accounts payable.

This is the operating reality for general contractors in 2026. Three forces are reshaping construction finance at the same time:

- A workforce shortage that is not going away

- Tariff and supply chain volatility that has become permanent rather than episodic

- An AI moment that is finally landing in the parts of the business where it can produce ROI

None of these are surprises. All of them are now showing up in the financials in ways that are harder to ignore. Here is what to track on each and why each one ties back to the same conversation about real-time financial visibility.

The Labor Squeeze Is Now a Financial Risk, Not Just an HR Problem

The labor shortage stopped being an HR story and became a finance story in 2026. The numbers underneath that shift, per the AGC and Sage 2026 Construction Hiring and Business Outlook:

- Additional workers the construction sector needs by 2033: 8.4 million

- Young people in the US who say they’re interested in the trade: 3%

- Firms struggling to find craft workers: 82%

- Firms struggling to fill salaried roles: 80%

- Firms that raised base pay 4 to 6% in the past year: 46%

The financial impact is higher payroll AND productivity volatility. Across the construction sector, productivity outcomes in the past year broke down roughly like this:

- Productivity gains: 32% of firms

- No change: 41% of firms

- Productivity declines: 24% of firms

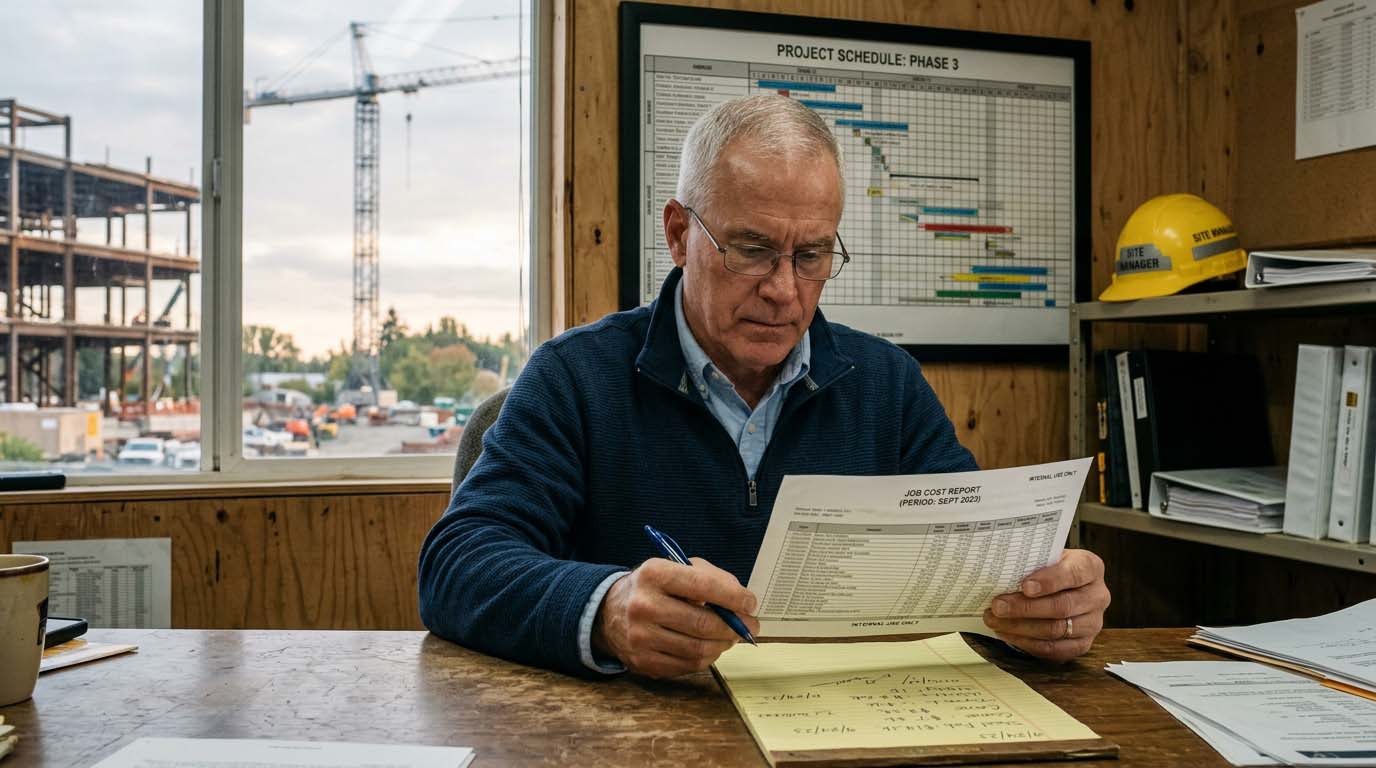

A GC that lost three weeks of crew time on a tight margin job can see a quarter of expected margin disappear before anyone notices. Workforce planning used to live in HR. In 2026 it lives in finance, because every labor decision now has a margin consequence that needs to be visible in the same cadence as the work itself. Contractors operating on monthly close cycles see labor variances show up in the financials a month too late to do anything about them.

The contractors that respond well are the ones who can see labor cost and productivity at the job level in real time. The ones that are slower to see it pay for the lag in margin.

Tariffs Are No Longer Background Noise

Through 2025, tariff policy moved from a periodic conversation into a structural input on construction cost. The AGC and Sage Outlook found that roughly 70% of construction firms reported being affected by tariffs in 2025. The downstream behavior changed accordingly:

- Passed costs through to owners: 35%

- Accelerated purchases to lock in pricing: 32%

- Absorbed costs into margin: 11%

The third row is the one to watch. Margin absorption is the path of least resistance in the moment and the most expensive choice over time. A GC absorbing even 1% of project cost on tariff exposure across an active portfolio gives back a meaningful slice of expected profit, and the visibility into how much has been absorbed often doesn’t show up until the project closes out.

The firms responding most effectively are doing two specific things:

- Running scenario modeling on commitment data weekly rather than monthly

- Pricing change orders against current cost rather than estimate cost

Both moves require financial visibility on a daily or near-daily cadence. Monthly close cycles do not produce decisions that keep pace with tariff volatility.

For a longer look at how labor shortages, inflation, and tariff volatility are reshaping construction tech decisions, see Navigating Inflation, Labor Shortages, and Tariff Volatility with Smarter Construction Tech.

Where AI Is Actually Producing ROI in Construction

The AI conversation in construction has been long on hype and short on adoption for several years.This year, that started to change in one specific area: finance and back office workflows.

The AGC and Sage Outlook found that 61% of construction firms either use AI today or plan to increase AI investment in 2026. Where AI is actually showing up in production environments is narrower than the headlines suggest:

- Office and administrative workflows: 45%

- Estimating: 23%

- Preconstruction and design: 20%

- Recruiting: 16%

The pattern in finance specifically is the strongest example of AI producing real ROI rather than experimental output. The workflows where AI tools have moved from pilot to production fastest:

- Accounts payable automation

- Invoice coding

- Approval routing

- Exception handling

The reason is structural: these workflows are high-volume, rule-driven, and the cost of error is contained. AI handles the routine 80% and surfaces the 20% that needs human judgment.

The contractors getting the most out of this are not the ones with the biggest AI investment. They are the ones with the cleanest underlying financial data. AI on a clean general ledger and a connected project budget produces useful output fast. AI on disconnected systems and manual data entry mostly produces faster versions of the same problems.

For a closer look at what AI in construction finance actually does in practice, see What Sage Copilot Actually Does (And Why Construction and Real Estate Teams Should Pay Attention) and ASG’s AI Commitments: AI You Can Actually Trust, Here’s How We Know.

The Common Thread: Real-Time Financial Visibility

The three forces above look like separate stories. They are actually one story told three ways.

- Labor productivity shows up in job cost data

- Tariff impact shows up in commitment data

- AI tools work best on clean, connected financial data

All three depend on the contractor’s ability to see what is happening across the financial system on the same clock as the work itself. A GC running on a monthly close cycle is reporting on labor productivity from four to six weeks ago, commitment data that may already be stale, and an AI environment built on top of data that needs reconciliation before it can be trusted. None of that is a recipe for responding well to the three forces reshaping the market.

The contractors that hold margin through 2026 are the ones that have already moved past monthly cadence in their financial reporting. That argument is the foundation of our pillar piece, The Real-Time Financials Every GC Needs to Protect Margin in 2026, which maps the four specific places GC margin leaks between closes.

Where Sage Intacct Construction Fits

The financial environment that supports labor visibility, tariff scenario modeling, and AI-ready data is one that posts field activity to the financial system within hours, reconciles committed against actual cost continuously, and runs consolidations across entities automatically.

Sage Intacct Construction is the cloud-native construction ERP built for that environment.

- AICPA’s preferred accounting solution

- 50,000+ construction businesses use Sage

- 48% of the ENR Top 400 contractors use Sage as their financial platform

For general contractors specifically, the platform supports:

- Real-time job costing tied to field activity

- Multi-entity consolidation that runs automatically

- Change order records tied directly to the project budget and the client contract

- Audit-ready WIP available on demand

- A foundation that AI tools (including Sage Copilot) can do useful work on without first requiring a data cleanup project

How GCs Are Preparing for the Rest of 2026

The contractors that move well through the rest of the year are doing three specific things differently:

- Pulling labor cost into job-level visibility on a weekly cadence rather than monthly. This puts the labor productivity story into the conversation while there is still time to act on it.

- Modeling tariff exposure on commitment data, not estimate data. Commitment data shows the cost of work already committed; estimate data shows the cost of work as bid. The first lets the team respond. The second tells the team what happened after the fact.

- Deploying AI tools inside their existing financial system rather than alongside it. AI inside an integrated ERP works on clean data. AI bolted onto a stack of disconnected tools amplifies the disconnects.

None of those moves require ripping out the existing tech stack. They require a financial system that operates on the same cadence as the work the contractor is actually doing.

Frequently Asked Questions

What is the construction labor shortage expected to look like through 2026 and beyond? The AGC and Sage 2026 Construction Hiring and Business Outlook projects the construction sector needs roughly 8.4 million more workers by 2033 to keep pace with demand, with only 3% of young people in the US expressing interest in the trade. In the near term, 82% of firms struggle to find craft workers and 80% struggle to fill salaried roles. The financial consequence is productivity volatility and wage inflation that contractors need to track on a weekly cadence to respond effectively.

How are tariffs affecting general contractor margin in 2026? Per the AGC and Sage 2026 Outlook, roughly 70% of construction firms reported being affected by tariffs in 2025. The most common responses were passing costs to owners (35%), accelerating purchases to lock in pricing (32%), and absorbing cost into margin (11%). Margin absorption is the most expensive long-term path because the cost shows up across an active portfolio and often does not surface until projects close out.

Where is AI actually being used in construction finance today? AI adoption in construction is concentrated in office and administrative workflows, where 45% of firms using AI are deploying it. AP automation, invoice coding, approval routing, and exception handling are the production-grade use cases. AI works best on top of clean, connected financial data, which means contractors with integrated ERPs are getting more value from AI tools than contractors running disconnected systems.

How does Sage Intacct Construction support labor cost visibility for general contractors? Sage Intacct Construction posts field activity to the financial system as the data is captured, which means labor cost shows up in job cost reports within hours rather than at month-end. Project budgets, change orders, and labor commitments are tied to live records that update together, so a productivity variance on a specific job shows up early enough for the project manager and finance team to respond.

What does Alliance Solutions do for general contractors navigating 2026? Alliance Solutions Group helps general contractors bring labor, materials, tariffs, and AI-ready financial data into one real-time financial view. The team configures Sage Intacct Construction to match how field and finance teams actually work, then provides ongoing support to keep the platform aligned as the business and the market change. Alliance is Sage’s number one Intacct partner in North America, with over 20 years dedicated to construction and real estate.

The Year Where Visibility Becomes the Standard

Labor, tariffs, and AI are not separate problems. They are three pressure points on the same financial function. The contractors that respond well in 2026 share one trait: they have built a financial system that produces decisions on the same clock as the work, not a month after the fact.

The rest of the year is going to reward contractors that see what is happening early enough to do something about it.

Take a self-guided product tour to explore Sage Intacct Construction at your own pace, or talk with one of our experts to see what a real-time financial stack looks like for a contractor your size.

How AI Is Quietly Changing Specialty Contractor Finance in 2026

How AI Is Quietly Changing Specialty Contractor Finance in 2026

A controller at a specialty contracting firm finishes Friday’s AP run. It used to take two days. This Friday it took four hours.

The AI tool that her accounting system added eighteen months ago is now coding 92% of invoices correctly on the first pass. She approves the exceptions. The rest moves through.

She is not running a futuristic operation. She is running an accounting team that adopted one specific AI tool inside an existing financial platform and trusted it to handle the boring 80% of the work. Her crew sizes did not change. Her customers did not change. The work the team is now able to do, because of the time AI gave back, did change.

This is the AI story most specialty contractors are not telling. It is not flashy. It does not involve robots on job sites. It involves boring back office workflows moving faster, more accurately, and with less staff effort than they did in 2024.

Here is where AI is actually showing up in specialty contractor finance in 2026, where it is not, and what to pay attention to as the technology matures.

Where AI Is Producing Real ROI in Construction Finance

The wins in 2026 are concentrated in three workflows where AI handles repetitive, rule-driven work that used to consume staff hours.

- Accounts payable: Invoice intake, GL coding, approval routing, exception handling — High-volume, rule-driven, contained cost of error

- Service ticket coding and billing readiness: Classifies tickets to the right job, contract, and billing window before they hit AR — Removes manual reconciliation that delays invoicing

- Financial reporting and anomaly detection: Flags unusual patterns in job cost data the day they happen — Early warning is the difference between a margin correction and a margin loss

The common thread across all three use cases: AI is helping specialty contractors compress the gap between work happening and that work showing up in the financial system. That gap is where revenue and margin slip for specialty contractors, which is the central thesis of our April pillar piece, Why Specialty Contractors Lose Money on Work They’ve Already Done. AI is one of the most direct levers for closing it.

Where AI Is Not Yet Living Up to the Hype

The same from the AGC and Sage 2026 Construction Hiring and Business Outlook data that shows AI working in finance also shows it struggling in other parts of specialty contractor operations:

- Office and administrative workflows: 45% — Production-ready; ROI is clear

- Estimating: 23% — Depends on judgment, relationships, project context

- Preconstruction and design: 20% — Workflows vary widely by firm and trade

- Recruiting: 16% — Tight labor market is a relationship problem, not a data problem

For specialty contractors specifically, the AI use case that’s furthest from production is field-side automation: technician diagnosis tools, route optimization, work documentation from the field. The early results are interesting. The production-grade version is not here yet for most trades.

The practical read on AI in specialty contractor operations is that 2026 is the year it produces real ROI in finance. Field-side ROI is closer to 2027 or 2028 for most trades. Specialty contractors that focus AI investment on the finance use cases first are going to capture the available value the soonest.

The Hidden Requirement: AI Needs Clean, Connected Data

The specialty contractors getting real value from AI in 2026 share one trait that has nothing to do with which AI tool they chose. They run on integrated financial systems where the underlying data is clean and connected.

- Clean, connected, real-time: Useful output fast

- Disconnected systems, manual entry, reconciliation lag: Faster versions of the same problems

A specialty contractor whose service work, install work, and maintenance contracts live in three separate systems will get marginal value from AI because the AI cannot make sense of data that the contractor’s own team has to reconcile manually. This is the gap that determines who gets ROI from AI investment and who gets a faster version of the same chaos. It is also why AI investment without underlying system investment tends to disappoint.

For more on what AI inside a construction financial system actually does, see What Sage Copilot Actually Does (And Why Construction and Real Estate Teams Should Pay Attention). For the broader question of how to evaluate AI tools for trust and reliability, see ASG’s AI Commitments: AI You Can Actually Trust, Here’s How We Know.

What Specialty Contractors Should Be Asking About AI

The right AI questions for specialty contractor finance teams are tactical, not strategic. Four questions that surface where the firm is and what comes first:

- How clean is our financial data? AI is downstream of data quality. A specialty contractor whose AP runs through Excel and email is not going to get useful AI output without first fixing the data flow. The investment in clean data pays for itself before any AI tool is deployed.

- Where is staff time actually going? AP processing, invoice coding, manual approvals, service ticket reconciliation, and inventory tracking are the highest-impact targets for AI inside specialty contractor finance. Mapping where staff hours go reveals where AI investment will pay back the fastest.

- Is our financial system AI-ready? Cloud-native systems with open APIs and structured data are AI-ready. On-premise legacy systems with custom data structures are not. Specialty contractors running on legacy software should answer the AI question alongside the platform question, not separately.

- Are we comfortable with how the AI was built? The AI tools that hold up over time are the ones built by vendors with clear policies on data handling, model training, and customer trust. Specialty contractors deploying AI on financial data should know what their vendor commits to before signing.

Where Sage Intacct Construction Fits

Sage Intacct Construction is the cloud-native construction ERP specialty contractors run when they want their financial system to support service work, install work, and maintenance contracts in one place. It’s also the platform where AI tools (including Sage Copilot) can do useful work without first requiring a data cleanup project.

For specialty contractors specifically, Sage Intacct Construction supports:

- AI-assisted automation in accounts payable, approvals, and routine billing

- Field activity flowing into real-time job costing as the work happens (gives AI current data to work with)

- Inventory following materials across trucks, warehouses, and job sites (gives AI accurate context)

- Multiple billing models inside the same system (no AI reconciliation across siloed tools)

Alliance Solutions Group configures Sage Intacct Construction around how specialty contractors actually run, not around how generic accounting software thinks they should. Take a self-guided tour of Sage Intacct Construction to see the platform that AI tools work on without scheduling a call.

A Quick AI Readiness Check for Specialty Contractors

Three questions that surface whether the firm is positioned to get real value from AI investment, or whether the AI question needs to wait for the platform question.

- Where does our financial data live? One system or several? Cloud-native or on-premise? Structured or improvised? Single answers point to AI readiness. Mixed answers point to a data and platform conversation first.

- How fast does field activity become billable data? Same day or end of week? Automated or manual? Mobile or paper? Faster, more automated, more mobile equals more AI-ready.

- Who owns the AI conversation? If the answer is “nobody yet,” that is the first thing to fix. AI without an owner inside the firm tends to be either oversold or ignored.

Frequently Asked Questions

Where is AI producing the most value in specialty contractor finance in 2026? According to the AGC and Sage 2026 Construction Hiring and Business Outlook, accounts payable automation, service ticket coding and billing readiness, and anomaly detection in job cost reporting are the three production-grade use cases. All three involve high-volume, rule-driven work that AI handles faster and more accurately than manual processes, which gives staff time back for higher-judgment work.

Why is AI not yet producing the same results in field operations? Field AI tools depend on the kind of variable, judgment-driven workflows that AI is still working out how to handle reliably. Estimating, design, and recruiting are also lower adoption rates because the work depends on relationships and context that AI tools have not yet matched. Most specialty contractors will see the field AI value in 2027 to 2028 rather than 2026.

Does AI work on a legacy accounting system? AI tools work best on cloud-native, integrated systems with clean structured data. Legacy systems with custom data structures, on-premise architecture, or significant manual reconciliation typically need a platform conversation before they need an AI conversation. Otherwise the AI investment produces marginal value.

What is the first AI use case a specialty contractor should deploy? Accounts payable automation is the most consistent first deployment because the ROI is fast, the data structure is well understood, and the cost of error is contained. Most specialty contractors see meaningful AP time reduction within the first few months of deployment.

How does Sage Intacct Construction support AI in specialty contractor finance? Sage Intacct Construction supports AI-assisted automation in accounts payable, approvals, and routine billing. The platform’s cloud-native architecture and connected data structure mean AI tools (including Sage Copilot) work on accurate, current data without first requiring a data cleanup project.

What does Alliance Solutions do for specialty contractors evaluating AI? Alliance Solutions Group helps specialty contractors evaluate where AI fits in their current financial system, where it does not, and what platform investment needs to come first. As Sage’s number one Intacct partner in North America with over 20 years of construction-only focus, the team works with the trade-specific realities of service, install, and maintenance operations.

The Quiet AI Era for Specialty Contractor Finance

The headline-grabbing AI use cases in construction are still mostly future tense. The quiet, ROI-producing AI use cases inside specialty contractor finance are already here. Contractors that focus their AI investment on AP automation, service ticket coding, and anomaly detection inside a connected financial system are the ones capturing real value.

The trade specifics depend on which kind of work the firm does most. Alliance has dedicated solutions for the trades where this conversation is loudest right now:

Fire & Life Safety Contractors

Take a self-guided product tour to explore Sage Intacct Construction at your own pace, or book a demo with one of our experts to see what AI-ready construction finance looks like for a specialty contractor at your size and stage.

Job Costing Visibility: How Dimensions Replace Spreadsheet Chaos for Electrical Contractors

Job Costing Visibility: How Dimensions Replace Spreadsheet Chaos for Electrical Contractors

The CFO wants to know which project type is most profitable before the next business development meeting. The answer should take thirty seconds to pull from the financial system. The controller runs the job cost report, sorts by project type, and stops. The commercial projects are coded three different ways across four different GL accounts. Healthcare has its own structure. The highway jobs use a fifth.

To compare margin across project types, she needs to export everything to Excel, manually map the overlapping codes to a common framework, and reconcile the differences. That is three hours of work before she can answer a thirty-second question. The CFO does not know the work is happening. The controller cannot skip it.

Every cost is recorded correctly. Every transaction is in the system. The problem is not what went in. It is how it is organized on the way out. A chart of accounts that accumulated over years of project managers, acquisitions, and shifting reporting requirements has no common structure. And a financial system with no common structure cannot answer a straightforward question without manual intervention.

How Charts of Accounts Get Out of Control

In a legacy system, every unique combination of reporting needrequires its own GL code. A labor cost on a commercial project in the downtown office is a different code from a labor cost on a residential job in the suburbs, which is different again from labor on a healthcare build. That logic compounds fast.

A small electrical contractor with twenty active projects, six cost types, and three departments can end up with hundreds of GL codes. Most of them overlap in meaning. Few of them compare cleanly across jobs. The chart of accounts was not designed for cross-job analysis—it was designed to record individual transactions, and that is all it does well.

The result is that every reporting question that crosses more than one job or one cost type requires manual work to answer. The data exists. Getting to it requires effort that belongs to the controller but produces no revenue for the company.

What a Dimension Is and Why It Changes the Equation

A dimension is a tag attached to a transaction. It is not a GL code. You do not need a new account for every reporting combination. You need one GL code and several dimensions that describe the transaction from multiple angles at once.

Instead of creating a unique GL code for commercial-labor-downtown-zone-three, you post to GL 5020 (Labor) and tag the transaction: Project \= Downtown Substation, Cost Type \= Labor, Department \= Commercial, Location \= Zone 3. The code stays clean. The reporting becomes fully flexible.

Inside Sage Intacct, every transaction can be tagged to multiple dimensions simultaneously: project, cost code, cost type, department, location, and more. Contractors who have made the switch find they can shrink their chart of accounts by half while gaining more granular reporting capability, not less. The accounts get simpler. The questions they can answer get more specific.

The Questions Dimensions Let You Answer

The real value of a dimension-based structure is not in how transactions are stored. It is in what becomes possible to ask.

Which jobs are running over on labor? Filter by cost type: labor, across all active projects. The answer comes from the data directly, not from a reconciled spreadsheet.

Which project manager is trending over budget? Filter by dimension: project manager. A pattern visible across one PM's jobs but not another's is a management conversation, not a mystery.

Which project type generates the highest margin? Filter by dimension: project type. If commercial healthcare returns better margin than ground-up residential, that is a business development insight with real strategic value.

Where are material overruns concentrated? Filter by cost code and cost type: materials. If copper is running over on the same project type repeatedly, the estimating assumption may be the problem, not the field.

None of these questions require a spreadsheet to answer. They require dimensions on the transactions and a reporting tool that can filter by them. That is the shift dimension-based accounting makes possible.

Dimensions Organize Good Data. They Cannot Fix Bad Data.

This is the part of dimension-based accounting that does not show up in a product demo. Dimensions are a reporting tool. They surface what is in the system. They cannot correct what was coded incorrectly, posted late, or never entered at all.

Change orders are a useful example. A change order with a vague or undocumented scope gets posted to a vague cost code. A dimension tag on that transaction reflects the vague code accurately. The reporting is clean. The data it is reporting on is not. Undocumented change requests produce undocumented cost entries, and no amount of dimension tagging makes an ambiguous posting queryable.

Timing matters in the same way. A change order that sits approved but unposted for three billing cycles eventually lands in the ledger—in the wrong period, tagged to the right dimensions. The cross-job margin report will show the cost in the month it posted, not the month the work happened. CO approval delays do not just slow cash flow; they distort the dimension-based reporting that depends on timely posting.

The same applies to field time entry. If labor hours are batched weekly and entered from a photo of a time card, the dimension tags on those entries reflect last week's job, not today's. Field data that posts daily carries current dimension tags. Batched field data carries dimension tags applied to work that is already history.

For electrical contractors implementing dimensions, the reporting capability is real. But it performs at the level of the data feeding it. Contractors who get the most value from dimension-based reporting are the ones who have also gotten disciplined about what goes into the system—correct cost codes, timely postings, and documented scope on every change. That is what makes the CFO's thirty-second question answerable.

Frequently Asked Questions

What exactly is a dimension in accounting software?

A dimension is a tag attached to a financial transaction that describes it from a specific angle—project, cost type, department, location, and so on. Unlike a GL code, which is a fixed account in the chart of accounts, a dimension can be applied to any transaction in any account. The same labor posting can carry a dimension for the project it belongs to, the cost type it represents, the PM responsible, and the geographic location—all at once. This enables multi-angle reporting from a single, clean set of transaction data.

How does dimension-based accounting reduce chart of accounts bloat?

In traditional systems, every unique reporting combination requires its own GL code. A contractor with ten project types, six cost types, and four departments might end up with hundreds of codes to accommodate every combination. With dimensions, you maintain one GL code per cost category and use dimension tags to carry all the context. The chart of accounts shrinks to a manageable set of true account categories. The reporting detail lives in the dimensions, not in the accounts themselves.

Can dimensions be added to an existing Sage Intacct setup, or does it require starting over?

Dimensions can be added to an existing configuration. New dimension values can be created and applied to transactions going forward without restructuring historical data. The most useful reporting comes from consistent tagging from the start of a project, but there is no technical barrier to introducing or refining dimensions mid-deployment. Contractors who implement dimensions mid-year typically apply them fully to new projects and do a partial cleanup on active jobs where reclassification is worth the effort.

What is the difference between a cost code and a dimension?

A cost code is a specific category within a project budget—typically tied to a scope of work like rough-in wiring, gear installation, or service labor. It is a line in the job cost structure. A dimension is broader and more flexible: it describes a transaction attribute that applies across all projects and cost codes, such as which project manager owns the work, which department it belongs to, or what project type it falls under. Cost codes tell you what the cost is for. Dimensions tell you who, where, and what kind—enabling comparisons that cut across the job cost structure.

How do dimensions help when a contractor is trying to identify which jobs are going underwater?

Without dimensions, spotting a problem job typically requires pulling individual job cost reports and comparing them manually. With dimensions, a controller can run a single report filtered by dimension—cost type, project manager, or project type—and see margin performance across the full portfolio at once. A job that is trending over budget on labor in week four is visible alongside every other job running the same pattern. Early visibility is what creates the opportunity to intervene before the overrun becomes a write-off.

See What Your Job Cost Data Should Look Like

If your team is spending weekends in spreadsheets to answer questions the financial system should be able to answer on its own, the issue is structure, not effort. Alliance Solutions Group works with electrical contractors to implement the dimension-based reporting that turns transaction data into management visibility.

Field to Financials: Why Your Job Cost Data Is Always Two Weeks Behind

Field to Financials: Why Your Job Cost Data Is Always Two Weeks Behind

A foreman on a Thursday afternoon has five electricians finishing rough-in on a commercial office build. Before he leaves the site, he tallies the week's hours from the time cards on his clipboard, writes the totals on a sheet, and texts a photo to the project coordinator. The coordinator forwards it to accounting. Accounting enters the hours on Monday.

By the time those hours hit the job cost ledger, the work is seven days old. If Monday is busy, or the photo is unclear, or accounting has pay applications going out, the entry slips to Tuesday or Wednesday. The foreman finished the work Thursday. The numbers appear in the system the following week.

This is not a failure of effort or attention. This is the standard process at most electrical contracting firms. And for contractors trying to manage job budgets, price change orders, and prepare pay applications from accurate numbers, the standard is a persistent problem: by the time the cost data is available, it is already wrong.

The Gap Is Structural, Not a People Problem

The accounting team is not slow. The foreman is not careless. The process was built around paper and weekly batches, and it performs exactly as designed. The problem is that the expectations around data have changed while the process has not.

Owners want tighter billing cycles. Project managers need to price change orders the same week a scope change happens. Controllers need WIP numbers that reflect the current state of the job, not last Tuesday's. The jobs have not slowed down. The data has to keep up.

Every step between the field and the financial system adds delay, and each delay compounds the others. A week of labor that has not posted is a week of cost invisible to everyone managing the job. Multiply that across a portfolio of active projects and the aggregate gap between what is happening and what the numbers show is substantial.

What Gets Decided on Stale Data

The cost of the lag is not abstract. It shows up in specific decisions made from incomplete inputs.

Pay applications. The monthly pay application is built from posted costs and earned revenue. If a week of labor and material receipts has not made it into the system by the time the pay app is assembled, that work does not get billed this cycle. It carries to next month, or gets caught in a revision that the owner's rep processes on their own schedule.

Change order pricing. A project manager pricing a change order from a cost report that is ten days old is building the estimate on last week's committed costs and labor actuals. How that plays out in margin is covered in Pricing Change Orders the Same Day: Why Accuracy Matters More Than Speed. The short version: the estimate is wrong before it is written.

WIP and forecasting. The percent-complete calculation driving WIP reporting depends on costs that have fully posted. If two weeks of labor and materials are missing, the job looks less complete than it is. The forecast overstates remaining margin. The controller is managing a number that does not reflect the actual job.

Crew and resource decisions. A PM deciding whether to add an electrician to a crew is asking that question against a job budget that may not include the last ten days of posted hours. The answer the cost report gives may not be the right answer.

Where the Lag Actually Lives

The delay does not come from one place. It compounds across four distinct hand-off points.

Time entry. Field hours are collected weekly, usually by foremen who aggregate time cards at the end of the week and submit them to the office. Best case, they are entered Monday. On busy weeks or when the submission is incomplete, they slip later. The lag is structural, not exceptional.

Material receipts. A purchase order goes out. Material arrives on site. The delivery receipt has to be matched to the PO and entered into the system. Each step is a separate action, often handled by different people. Until the receipt is matched and entered, the material cost is a commitment—visible on the PO, not posted to the job as actual cost.

Subcontractor billing. Subs invoice on their own schedules. Until the invoice arrives, is reviewed, and is approved for entry, the subcontractor's cost does not appear in the job cost ledger. On jobs with multiple subs, this can represent a significant share of total cost that is simply not visible until billing happens.

Daily logs and field notes. Field observations, productivity notes, and daily reports often live in informal channels: texts, photos, a foreman's notebook. They rarely make it into the financial system at all. The cost picture is missing the context that explains why the numbers are what they are.

What Changes When Field Data Posts the Same Day

The fix is not to make the accounting team work faster. It is to remove the manual steps that introduce delay in the first place.

When field crews log time directly from a mobile app at the end of each shift, that entry flows into Sage Intacct the same evening. No photo, no forwarded email, no Monday batch entry. The foreman submits from the job site. The hours are in the ledger that night. A PM checking the job cost report the next morning sees yesterday's labor, not last week's.

When a purchase order is issued, the committed cost appears on the job immediately—before the invoice, before the delivery receipt. The job cost report shows what is spoken for on the project, not just what has been billed and matched. A controller preparing the pay application is working from a full picture of obligations, including material that has been ordered but not yet invoiced.

For electrical contractors managing multiple active jobs, this shift changes the nature of the job cost review. The question stops being what happened two weeks ago and starts being what is happening now. That makes the data useful in real time: for change order decisions, for crew planning, and for the pay application that closes at the end of the month.

When job cost data is current, it also becomes the foundation for the reporting and analysis that gives management real visibility into profitability across the portfolio. How that dimension-based reporting works in practice is the subject of Job Costing Visibility: How Dimensions Replace Spreadsheet Chaos for Electrical Contractors.

Close the Field-to-Financial Gap

If your team is making job decisions from a cost report that is a week or more behind the actual job, the margin impact is showing up somewhere—in short pay applications, in stale CO estimates, or in WIP reports that do not reflect what the job is actually doing. Alliance Solutions Group works with electrical contractors to replace manual batch workflows with real-time field-to-financial data.

→ Take a self-guided product tour

Frequently Asked Questions

How long does it typically take for field time entries to post to the job cost ledger in a manual process?

In a typical manual workflow, field hours collected Friday reach the ledger on Monday at the earliest. When submissions are incomplete, photo quality is poor, or the accounting team has competing priorities, the entry slips to Tuesday or Wednesday. A seven-to-ten-day lag between hours worked and hours posted is common. On jobs where a pay application coincides with the week's close, the delay can extend further as accounting prioritizes billing over entry.

What is the difference between a committed cost and an actual cost in job costing?

A committed cost is an obligation already incurred but not yet invoiced or paid—most commonly a purchase order that has been issued. An actual cost is a transaction that has posted to the ledger, typically from a received and matched invoice. Both matter for job cost accuracy. A contractor who tracks only actual costs is missing the full picture of what the job has spent and committed. Committed cost visibility, available the moment a PO is issued, closes that gap before the invoice arrives.

How does job cost data lag affect the accuracy of a monthly pay application?

Pay applications are built from posted costs and earned revenue. If a week or more of labor entries and material receipts have not made it into the system by the time the pay app is assembled, that work is not included in the billing cycle. The pay application goes out short. The contractor has done the work and incurred the cost but has not captured the revenue. That shortfall either carries to next month or requires a revision, both of which slow cash flow and add administrative burden.

Is same-day time entry realistic for field crews on a busy electrical job?

Yes. Daily time entry via a mobile app takes a few minutes per crew member and is typically completed before leaving the job site—similar to the time it already takes to fill out a paper time card. The barrier is habit and process change, not the time required. Contractors who have made the switch report that foremen adapt quickly once they see that the data from Monday's entry is visible to the PM on Tuesday morning rather than the following week.

Does faster field data entry also help with change order documentation?

It does. When field time and material costs post daily, a project manager pricing a change order has access to current committed costs and labor actuals on the job—not a snapshot from ten days ago. The estimate is built from data that reflects the real state of the project on the day the change is priced. That accuracy is the foundation of defensible CO pricing, and it depends entirely on how current the underlying data is.

Change Order Aging: Why Approved COs Quietly Lose Money in Electrical Contracting

Change Order Aging: Why Approved COs Quietly Lose Money

The pay application goes out on the 25th. It looks short. The controller pulls the job cost report and finds nine change orders that were approved weeks ago and never posted to the GL. Two are more than a month old. Both will miss this billing cycle.

The COs were priced correctly. The owner signed off. The work is done. None of that moves money until a CO becomes a posted, billable line on a pay application, and these are not.

This is the change order problem nobody talks about. It is not slow pricing. It is not bad estimating. It shows up after the estimate is right and the approval is signed. It lives in the gap between approved and posted. That gap has a name: aging. And for electrical contractors running active portfolios with dozens of changes per job, CO aging is one of the most expensive invisible line items on the schedule.

The Change Order Does Not End When It Is Priced

Most conversations about change orders focus on speed to price, getting the number in front of the owner quickly and moving on. Getting that price right from accurate, current job data is the necessary first step. But the work after approval gets far less attention, and it is where the margin actually shows up or disappears.

A priced CO has to be submitted, approved by the owner's rep, signed, posted to the job cost ledger, and rolled into the next pay application. Every one of those steps is a handoff. Every handoff is a place where a CO can sit.

In a healthy process, the gap between priced and posted is a few days. In most contractors' real-world workflows, it is two to four weeks. Sometimes longer.

Why Aging Is the Right Way to Think About It

AR teams have been tracking invoice aging for decades. The logic is simple: the older an unpaid invoice gets, the less likely it is to be collected in full. Buckets at 30, 60, 90, and 120 days drive collection priorities.

Change orders deserve the same discipline. CO aging is the time between when a CO is priced and when it is a posted, billable line on the job. The longer that window, the more risk piles up.

Owners forget the context behind the change, and disputes get easier. Field conditions shift, and documentation becomes harder to assemble. Subcontractor markups stack—nested COs from subs sit because yours is sitting. And cash that should be in your pay application is not.

For electrical contractors, the volume problem makes this worse. A single job can generate dozens of small COs across the life of a project. Nested COs from subs amplify the count. If even a quarter of those age past two weeks, the aggregate cash drag adds up fast.

What Aging COs Actually Cost

The visible cost is unpaid work. The hidden costs are harder to spot until they show up in a quarterly review.

Cash flow. Revenue earned but not invoiced is revenue not financing the job. Pay applications go out short. Working capital tightens. The contractor borrows to cover what should already be billable.

Job costing accuracy. WIP reports understate revenue and overstate variance until the CO posts. Anyone looking at the job before posting sees a worse picture than reality. Bad data drives bad decisions.

Forecasting. PMs run one number in their heads. Accounting runs another. The owner sees a third. None of them line up until the CO clears.

Owner pushback. A CO submitted within a week of the change is easy to defend. A CO submitted three weeks later, after the work is done and the cost is sunk, invites scrutiny. Some get reduced. Some get rejected.

Subcontractor friction. When your CO sits, your sub's CO sits. They feel the delay in their pay application. The next time you negotiate, that memory is in the room.

The Four Reasons COs Age

Most aging COs trace back to one of four causes. Each has a structural fix.

1. Documentation gaps. The CO is priced, but the supporting field documentation is incomplete. Photos, time entries, signed RFIs, or T\&M tickets are missing. The owner's rep asks for more, and the CO goes back.

The fix is tying field documentation directly to CO creation so the package is complete before it leaves the field. That principle starts with how change requests are documented in the first place.

2. Approval chain ambiguity. Nobody knows who signs next. A CO sits in an owner's inbox because three people think someone else is reviewing it. The fix is a pre-defined approval workflow for every project, agreed at kickoff and built into the system.

3. The accounting handoff. The PM marks a CO approved. The post to the GL still has to happen. If that step lives in a manual email, the CO sits until someone in accounting has time. The fix is real-time integration between project tools and the general ledger so posting is automatic, not a task on a to-do list.

4. No visibility into aging. Nobody is watching aging until it becomes a problem. By the time a CO crosses 30 days, the cost is already real. The fix is a live view of every open CO with days-since-priced as a sortable column. If a PM can see that CO 14 has been sitting for eleven days, they can make a phone call. If they cannot see it, they cannot act on it.

How a Modern Construction ERP Closes the Aging Gap

Most of these causes are structural, which means procedural fixes like more follow-up emails and more check-ins only go so far. The more durable fix is a system that removes the manual handoffs.

Inside Sage Intacct construction, CO aging is a managed metric, not a quarterly surprise. Every open change order carries a live aging counter visible at the line level, the job level, and across the full portfolio—sortable by PM, by project, by days outstanding. When an owner approves a CO, that status flows to the GL automatically without a manual email or batch entry in between. T\&M changes close faster because field time posts to the job daily rather than in a weekly batch that can miss a billing cycle. The result is a CO dashboard that tells a PM exactly which approvals to chase before the pay application closes.

For electrical contractors specifically, the volume problem matters. Hundreds of small COs across a busy portfolio are not unusual. Tracking them in spreadsheets or across two disconnected systems is where aging compounds. One system, one source of truth, one set of numbers everyone trusts.

What a Healthier CO Process Looks Like

A contractor with CO aging under control runs the process on three principles.

Target aging windows are defined upfront. A reasonable target is seven days from priced to owner approval, two days from approval to posting. That gives a worst case of roughly nine days from price to billable. Without a target, aging is not a metric. It is just a byproduct of however long things happen to take.

Aging is reviewed weekly, not when someone notices a problem. A standing PM and accounting meeting that opens with the CO aging report turns aging into a managed metric instead of a quarterly surprise. If a CO has been sitting for eleven days without owner sign-off, someone needs to make a call, not find out at month close.

PMs and accounting share one number, in one system. When the project management view and the GL view show different CO statuses, someone is working from bad data. The single source of truth is the difference between a CO process that protects margin and one that bleeds it quietly across the year.

"Manual processes push change order turnarounds to 60 to 90 days. And it is a pretty common practice in construction: if you are not billed within 90 days of a change order being identified, the owner does not have to pay it."— Spencer Doak, Account Executive, Alliance Solutions Group

Get CO Aging Under Control

If your team is chasing CO approvals through email, posting to the GL once a week, or finding out about aging only when an owner pushes back, there is a better way to run this. Alliance Solutions Group works with electrical contractors to get CO workflows under control using the visibility and structure needed to keep aging short and margins protected.

→ Take a self-guided product tour

Frequently Asked Questions

What is change order aging?

CO aging is the time elapsed between when a change order is priced and when it posts as a billable line to the job. The longer that window stays open, the greater the risk of missed billing cycles, owner disputes, cash flow drag, and WIP reporting that understates where the job actually stands. Most electrical contractors do not track CO aging as a metric, which means the problem accumulates quietly until it shows up in a quarterly review or an owner pushback.

What is the 90-day contractual billing window, and does it apply to most electrical contracts?

Many construction contracts include a provision that limits the owner's obligation to pay for work not billed within 90 days of identification. If a change order is priced in week one, sits through approval delays, misses two pay applications, and is finally submitted at day 95, the owner may not be legally required to pay it. That’s a contract enforcement question, not a billing dispute. The specific language varies by contract, but the 90-day window is common enough that CO aging directly affects whether approved work gets paid. Contractors should confirm the billing provisions in each contract at project kickoff.

What is a realistic target aging window for change orders?

A reasonable target for most electrical contractors is seven days from priced to owner approval, two days from approval to GL posting. That puts the worst-case gap at roughly nine days from estimate to billable line. Contractors who hit that target consistently find that owner disputes drop, WIP accuracy improves, and pay applications go out fuller. The specific targets will vary by project size and owner sophistication, but any target is better than no target.

How does an aging CO affect WIP and job cost reporting?

Until a CO posts to the job cost ledger, the revenue it represents does not appear in WIP. The job looks less complete than it is. Cost-to-date looks worse relative to budget. The over-under calculation that drives billing decisions is working from an incomplete picture. Anyone reading the job cost report, whether it is a controller, PM, or CFO, is seeing an understated revenue position. Decisions made on that data, including pay application amounts, are decisions made on bad inputs.

What is the most common cause of CO aging in electrical contracting?

In most operations, it is the handoff between project management and accounting. The PM marks a CO approved. The GL post is a separate step that is often handled through a manual email, spreadsheet update, or periodic batch entry. Until someone in accounting acts on it, the CO is approved in theory but unposted in reality. The field and the office are tracking different statuses on the same CO. Closing that handoff through real-time integration between the project system and the general ledger removes the most common single point of delay.

Pricing Electrical Change Orders the Same Day They Happen

Pricing Change Orders the Same Day: Why Accuracy Matters More Than Speed

A project manager gets a scope change notification on a Tuesday morning. A wall needs to move. The electrical rough-in has to be re-run. The owner wants a number by end of day.

The PM opens the spreadsheet. It was last updated eleven days ago. Labor rates have been renegotiated since then. The copper pricing in the master file reflects last month’s market. The PM knows the numbers are a little off, but the gap feels manageable. Close enough.

The CO goes out. The owner accepts it. Work starts Wednesday.

Three weeks later, the job cost report shows that CO running six percent margin against a bid of eleven. The shortfall is not a labor overrun. The crew executed cleanly. The materials came in on scope. The margin disappeared because the price was built on data that was already wrong when it was submitted.

This is not a rare outcome. For electrical contractors pricing change orders from spreadsheets, it is the expected one.

The Problem Is Not How Fast You Price It. It Is What You Price It From.

Most conversations about change order performance focus on cycle time: how quickly a CO gets approved, how fast it moves through the chain. Speed matters, but it is a secondary problem.

The first problem is accuracy.

An electrical change order is only worth what the price can support. If the labor rate in the estimate is stale, the margin in the estimate is wrong. If the material pricing reflects last month’s market rather than this week’s purchase orders, the bid is not a real number. The owner accepts it at face value. The job runs at actual cost. The contractor absorbs the difference.

For electrical contractors, two cost categories move fast enough to matter: labor and materials. Union and non-union rates adjust on agreement cycles that do not align neatly with project billing cadences. Copper, conduit, and prefabricated assemblies move with commodity markets. A spreadsheet that has not been touched in eleven days is not a pricing tool. It is a historical record.

The compounding effect is where the real damage accumulates. A single CO priced $1,800 low on a $50,000 change represents 3.6 percent of margin given back before work starts. Multiply that across twenty or thirty change orders on an active job and the aggregate shortfall is significant. It’s not one bad decision, it’s a pattern of small decisions made against inaccurate inputs.

Where the Inaccuracy Comes From

The root cause is structural. Most electrical contractors maintain pricing data in spreadsheets that are updated manually, on someone’s schedule, which is not daily. That spreadsheet is disconnected from the job cost ledger, from the purchasing system, from the commitments already posted on the job.

When a PM sits down to price a CO, they are working from a static snapshot. The job is a live document. The snapshot is not.

In practice, the disconnect looks like this: A foreman flags an additional scope item on Monday. The PM gets the notification Tuesday. They open the master pricing file and see it was last updated eight days ago. Labor rates were revised on Thursday. Materials were purchased Friday at a different price than the file reflects. The CO estimate is built on inputs that were already behind reality before the first number went in.

The faster a CO needs to go out, the worse this problem gets. Speed pressure pushes PMs toward the most available data, which is usually the least current.

What Accurate, Same-Day CO Pricing Actually Requires

The goal is not to price change orders faster. The goal is to price them right, from data that reflects the actual state of the job on the day the change is priced.

That requires the pricing tool to be connected to the same data source the job cost ledger uses. Not a separate spreadsheet that gets updated when someone gets around to it. The live ledger.

When labor rates update, they should update everywhere at once: in the job cost tracking, in the estimate templates, in the CO pricing workflow. When a purchase order is issued for materials, that committed cost should be visible to the PM pricing the next change on the same job.

Inside Sage Intacct, change orders are priced against the live job ledger rather than a standalone spreadsheet. Current labor rates, committed material costs, and existing budget data pull into the CO estimate from the same source the accounting team is working from. The PM submitting the CO and the controller reviewing the job cost report are looking at the same set of numbers at the same moment.

That alignment is what makes the price defensible. Not because the PM worked faster, but because the estimate was built on accurate inputs.

The Change Request Is the Foundation

Accurate CO pricing depends on accurate documentation of what changed. A PM who prices a change based on a verbal description from a foreman is working from an incomplete input. A PM who prices from a formal change request, where scope, cost impact, and schedule impact are already documented, is working from a complete picture.

The change request step creates the record that the CO pricing is based on. Without it, the number is a guess dressed as an estimate. For a deeper look at why that documentation gap is so costly, see Why Electrical Contractors Lose Money on Undocumented Change Requests. The traceability matters most when the owner questions the number four weeks after the work is done.

A Correct Price Is Step One

Getting the CO price right is the beginning of the process, not the end. A CO priced accurately still needs to be submitted, approved, posted, and rolled into the next pay application. Every step between the estimate and the billable line is a place where margin can disappear. Accurate pricing and a fast, clean posting process are both required. Neither is sufficient on its own.

The contractors who protect margin on change orders do both: they price from current data and they move the CO through the approval and posting workflow without letting it sit. One without the other still produces margin loss, just at a different point in the process.

If your team is pricing change orders from a spreadsheet that is more than a week old, the margin shortfall is probably visible in your job cost reports. Alliance Solutions Group works with electrical contractors to close that gap, starting with the data that feeds every estimate.

→ Take a self-guided product tour

Frequently Asked Questions

What does 'pricing data' mean in the context of a change order estimate?

For an electrical contractor, the two inputs that move fast enough to matter are labor rates and material costs. Labor rates shift on union agreement cycles and can change mid-project. Material costs, particularly copper, conduit, and prefabricated assemblies, move with commodity markets and recent purchase orders. A CO estimate is only as accurate as these two inputs on the day the estimate is built. Everything else in the calculation can be perfectly accurate and the margin will still be wrong if those two numbers are stale.

How outdated does pricing data need to be before it affects CO margin?

That depends on how fast your costs are moving. On a job with active material purchasing and recent rate changes, even a week-old spreadsheet can carry inaccuracies large enough to matter. The problem is rarely a single large error. It is a pattern of small ones that compound across twenty or thirty change orders on a busy job. A single CO priced $1,800 low on a $50,000 change is a 3.6-percent margin give-back before work starts. Across a full project, those gaps add up.

What is a change request, and why does it come before a change order?

A change request is the internal documentation of a scope change before a price is attached to it. It captures what changed, why, and what the field impact is. A change order is the priced and submitted version that goes to the owner. Pricing a CO without a formal change request means the estimate is built on a verbal description rather than a documented scope, which creates traceability problems when the owner questions the number after the work is done.

Does pricing from live job data mean the PM is not estimating anymore?

No. The PM still builds the estimate using quantity takeoff, labor hours, and markup logic. What changes is the inputs feeding that estimate. When labor rates and committed material costs pull from the live job ledger rather than a static spreadsheet, the estimate starts from an accurate baseline. The judgment and expertise still belong to the PM; the data those judgments depend on is just current.

Why do owners push back more on change orders submitted after the work is done?

By the time a CO is submitted post-completion, the owner has already seen the finished result. The urgency is gone. Documentation is harder to assemble and easier to challenge. Disputes over scope, timing, and cost are more common when the CO follows the work instead of preceding it. Submitting promptly and using accurate data keeps the number defensible at the moment it matters most.

Customer Testimonials